Understanding the Mobile Wallet

It used to be that “cash was king,” but many consumers today — especially millennials — rarely carry paper money, and even the idea of using credit cards is an archaic concept to some. In the 21st century world that we live in, mobile payment apps are the way more and more people like to pay for things.

In fact, a recent study by Javelin projected mobile payments would increase to 410.5 billion by 2020.

After all, “the mobile wallet” is more convenient, charge less fees than credit cards and take seconds to process. Security on these apps is also very strong.

And they are simple to use. All one needs to do is download a free app, upload the numbers of their major credit and debit cards and “tap to pay” with a phone at any retailer who accepts the service.

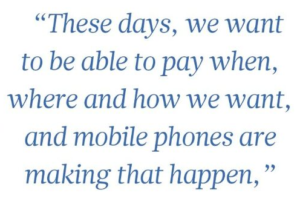

“These days, we want to be able to pay when, where and how we want, and mobile phones are making that happen,” says Zahir Khoja, SVP of global acceptance at Mastercard, which has started to roll out its own mobile payment app. “They have become an essential, ever- present part of our daily life. According to eMarketer, American adults were expected to spend an average of three hours, 35 minutes a day on their mobile device, and many of us are choosing the convenience, simplicity and speed of paying with our digital wallets.”

Many cities are even turning to mobile payments for transit, making “tap and go” second nature to millions, who are coming to expect the same simple payment experience wherever they pay.

Still, many small retailers in the U.S. have been slow to embrace the technology.

“Every retailer wants his or her customer to leave happy and look forward to shopping there again — and for specialty store owners who want to thrive in the face of growing online competition, giving customers a quick and safe way to pay is one way to stay competitive,” Khoja says. “Millennials are also much more likely to use mobile payments, and as their buying power grows, so will the need for retailers to give them the flexibility they seek.”

Acrylic Tank Manufacturing, Las Vegas, Nevada, does tours of hundreds of guests a day who travel from all across the world to see ATM (the home of the TV show, Tanked) and have a very active gift shop selling T-shirts, memorabilia and more.

“Mobile payments are especially important for us as we are still a small business, but have international visitors and customers, and many of them are used to using mobile payment apps in their countries,” says Victor Jackson, retail manager for the store. “We have found more and more people choose to pay this way, and I feel people are more likely to buy an impulse item because it’s so easy.”

Alex Tran, a digital marketing strategist at Hollingsworth, a Dearborn, Michigan based supply chain company, works with more than 300 vendors that use various payment software and apps to process their transactions. He notes that mobile payments apps have revolutionized how people buy and sell items since it first took off in 2010.

“Mobile payment options increase sales, and there are numerous studies showing this, and it is technology that is only growing,” he says. “The pros for a retailer are there is less cash to handle and thus less money lost if your store were to get robbed or if you lose your cash somehow. Plus, it’s convenient and you are receiving sales that would have been lost had you only accepted cash.”

How it Works

The most popular mobile payment apps are Apple Pay, Google Pay (formerly Android Pay), Square and Samsung Pay. Then there’s PayPal, which acquired Venmo six years ago, and last year along saw more than $50 billion in transaction from the app. That one though, is more about peer-to-peer money sharing, though it does work at some stores as well.

Tran explains that these all work similarly. Mobile payments are processed on the phone or a tablet and the app is usually used with a credit card swiper. “Nowadays, consumers can use NFC, a picture can be taken of a credit card, or the seller can manually enter the card details into the app,” he says. “A retailer would enter their product codes/inventory into the app. When someone makes a purchase, the retailer will find the item in the app and then total up the sale. The retailer will then process the payment by swiping the card and then a digital receipt will be sent to the buyer. It can also be printed if the retailer has a printer that works with the app.”

Mobile phones and other connected devices that house digital wallets use radio frequency technology to “talk” to a similarly-enabled store reader.

“You load your payment card information into the digital wallet of your choice on the device of your choice, from mobile phones to fitness bands to smartwatches,” Khoja says. “Then you simply tap your device on the store’s reader, and the payment information stored in the digital wallet is transmitted instantly and securely.”

In the case of Mastercard, the company leverages tokenization technology called MDES (Mastercard Digital Enablement Service), which replaces the consumers’ payment details with a randomly-generated “token” so the actual account information is never shared.

Retailers are charged a fee each time a consumer uses a credit card at checkout, but the mobile payment apps have lower payment processing fees in most cases. Paypal and Square will offer their square card readers for free, but there is a fee with every sales transaction.

Paypal charges a percentage (around 4%) and Square charges a fee per transaction plus a percentage of the sale. Meanwhile Apple Pay, Google Pay and Android Pay all require stores to install a contactless payment–capable point-of sale terminal (usually around $500) but none charge any fees per transaction.

Marketing Matters

At the Acrylic Tank Manufacturing store, there are signs at the counter and throughout the aisles showing that the store accepts mobile payments. Jackson notes this is important because it lets the customers know that they can easily pay for what they find and it encourages more purchases.

Tran also believes that if a customer knows they can pay with a mobile payment app, they will be more inclined to purchase due to the convenience.

“It offers a convenience to the customer shopping,” he says. “Plus, eventually a brick and mortar store can transition into an e-commerce store and both Paypal and Square can easily be integrated into a platform of your choosing.”